Small and medium-sized merchants often face cash flow gaps that hinder growth, from purchasing inventory to covering unexpected expenses. Traditional bank loans can take weeks or months to secure, with rigid repayment terms that don't flex with your sales. For businesses using Clover POS systems, working capital solutions offer a faster, more flexible alternative. These financing options leverage your daily credit card processing data to provide quick access to funds, with repayment automatically tied to your sales volume. This guide walks you through applying for working capital with Clover in 2026, covering eligibility, application steps, and repayment management to help you make informed funding decisions.

Table of Contents

- Understanding Working Capital Options With Clover POS

- Preparing Your Clover Account And Business For Working Capital Application

- Step-By-Step Guide To Apply For Working Capital With Clover Capital

- Troubleshooting Common Issues And Managing Repayments Efficiently

- Discover Flexible Working Capital Solutions With Clover Capital

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Fast approval process | Working capital loans up to $250,000 can be approved in under 72 hours with repayment tied to daily sales. |

| Flexible repayment structure | Repayment is a percentage of daily credit card sales processed on Clover terminals, usually 8% to 20%. |

| Clear eligibility requirements | Eligibility requires an active Clover account, minimum processing history, and a U.S.-based bank account. |

| Factor rates vs. interest | Merchant cash advances differ from traditional loans by using factor rates instead of interest and flexible repayment. |

| Cash flow assessment needed | Careful review of terms and business cash flow needs is essential before applying. |

Understanding working capital options with Clover POS

Working capital represents the funds available for your daily business operations, from paying suppliers to covering payroll. For merchants using Clover POS systems, accessing this capital quickly can mean the difference between seizing growth opportunities and missing them entirely. Clover Merchant Cash Advances provide an immediate lump sum that you repay through a percentage of your daily card transactions, eliminating the pressure of fixed monthly payments.

Unlike traditional loans with interest rates and set payment schedules, merchant cash advances use factor rates to determine your total repayment amount. A factor rate of 1.3 means borrowing $10,000 requires repaying $13,000 total. This structure offers predictability in your total cost while maintaining flexibility in daily repayment amounts based on actual sales performance.

The holdback percentage determines how much of each credit card transaction goes toward repayment. Typical holdback ranges from 8% to 20% of your daily credit card sales. If you process $1,000 in card sales today with a 15% holdback, $150 automatically goes toward your advance repayment. On slower days with $500 in sales, only $75 is collected.

This sales-based repayment model offers several advantages for Clover merchants:

- Approval decisions happen in under 72 hours based on processing history rather than credit scores

- No fixed monthly payments that strain cash flow during slower business periods

- Automatic deductions from card sales eliminate manual payment tracking

- Higher sales volumes accelerate repayment, reducing the total time you're carrying the advance

Pro Tip: Before applying, analyze your sales patterns over the past six months to identify your slowest periods. Calculate what a 15% holdback would mean during those times to ensure you maintain sufficient operating capital even when sales dip.

Preparing your Clover account and business for working capital application

Successful working capital applications start with proper preparation. Meeting eligibility criteria ensures your application moves quickly through approval without delays or rejections. Most providers require an active Clover account with consistent credit card processing history, typically at least three to six months of transaction data. Your business must operate in the United States with a U.S.-based business bank account for fund deposits and potential backup repayment.

Sales volume plays a crucial role in determining both eligibility and advance amounts. Providers analyze your monthly credit card processing to assess how much capital your business can support. Higher consistent volumes typically qualify for larger advances, while volatile or declining sales may limit approval amounts or result in rejections.

Gather these essential documents before starting your application:

- Recent Clover processing statements showing at least three months of transaction history

- Business bank account information including routing and account numbers

- Business formation documents such as your EIN and articles of incorporation

- Owner identification including driver's license or passport

- Business contact information and physical location details

Review your Clover Capital repayment options to understand how different holdback percentages impact your daily operations. A 10% holdback leaves more cash available for immediate expenses but extends your repayment timeline. A 20% holdback accelerates repayment but requires stronger daily sales to maintain sufficient operating capital.

Check your average monthly card sales through your Clover dashboard. Most providers offer advances ranging from 50% to 100% of your average monthly processing volume. If you consistently process $30,000 monthly in card sales, you might qualify for advances between $15,000 and $30,000 depending on the provider's risk assessment.

Pro Tip: Update your Clover account information and bank details at least one week before applying. Outdated contact information or banking details can delay approval and funding by several days while providers verify current details.

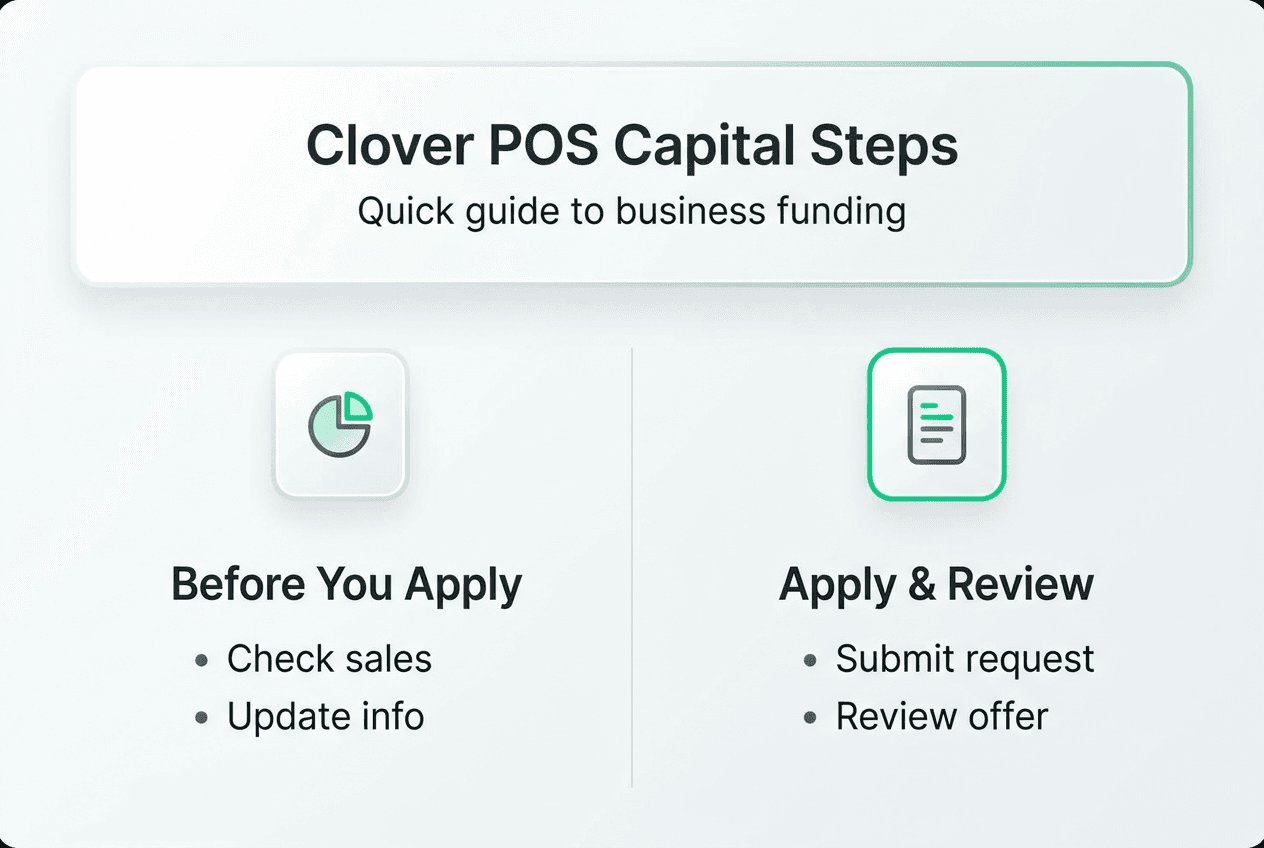

Step-by-step guide to apply for working capital with Clover Capital

Applying for working capital through Clover-based providers follows a straightforward process designed for speed and simplicity. Here's how to navigate each stage:

-

Log into your Clover POS dashboard and review your sales metrics. Verify your account shows active status with consistent processing history. Check that your business information, including legal name, address, and contact details, matches your official business records exactly.

-

Visit the Clover Capital partner platform or authorized provider website. Complete the online application form with your business details, requested funding amount, and processing history. Most applications take 10 to 15 minutes to complete with all documents ready.

-

Review the offer terms carefully, including the factor rate and holdback percentage. Funding amounts are based on monthly credit card volume, often up to 100% of average sales. A factor rate of 1.3 means $10,000 borrowed requires $13,000 repayment, so calculate your total cost before accepting.

-

Provide consent to terms and authorize the provider to access your Clover processing data for underwriting. This data-driven approach enables faster decisions without extensive financial documentation or credit checks.

-

Await approval, typically delivered within 72 hours or less. Once approved, funds transfer to your business bank account as a lump sum, often within one business day. Repayment begins automatically through daily holdbacks from your card sales.

This table illustrates how factor rates impact total repayment on sample advance amounts:

| Advance Amount | Factor Rate | Total Repayment | Effective Cost |

|---|---|---|---|

| $10,000 | 1.25 | $12,500 | $2,500 |

| $10,000 | 1.30 | $13,000 | $3,000 |

| $10,000 | 1.40 | $14,000 | $4,000 |

| $25,000 | 1.30 | $32,500 | $7,500 |

| $50,000 | 1.35 | $67,500 | $17,500 |

Compare these costs against your expected revenue from using the capital. If a $10,000 advance with a $3,000 cost enables you to purchase inventory that generates $8,000 in profit, the financing makes business sense. If the same advance only generates $2,000 in additional profit, you're losing money on the transaction.

Pro Tip: Request quotes from multiple providers before accepting an offer. Factor rates can vary significantly between lenders, and comparing terms helps you avoid surprises while securing the most favorable financing for your situation.

Troubleshooting common issues and managing repayments efficiently

Even with proper preparation, merchants sometimes encounter obstacles during application or repayment. Understanding common issues helps you address them quickly and maintain smooth operations.

Eligibility rejections often stem from insufficient processing history, declining sales trends, or existing cash advance balances with other providers. If rejected, request specific feedback on why your application didn't qualify. You may need to wait until you've built more processing history or improved sales consistency before reapplying.

Misunderstanding holdback rates creates cash flow problems when merchants don't account for daily deductions. Repayment terms and holdback rates vary by issuer, so review your merchant agreement carefully. Calculate what your holdback percentage means in actual dollars during typical, high, and low sales days.

Cash flow challenges emerge when businesses take advances without assessing whether their sales patterns support the holdback structure. Sales volatility significantly impacts MCA suitability, so businesses with inconsistent revenue should evaluate whether this financing model fits their operations.

Follow these best practices to manage repayments effectively:

- Monitor daily sales and holdback deductions through your Clover dashboard to track repayment progress

- Maintain a cash reserve equal to at least two weeks of operating expenses separate from daily sales

- Avoid taking multiple advances simultaneously unless your sales volume clearly supports overlapping holdbacks

- Plan major purchases or slow seasons around your repayment schedule to prevent cash shortages

- Communicate with your provider immediately if you anticipate repayment difficulties rather than waiting for problems to escalate

Before applying for any merchant cash advance, thoroughly assess whether the financing structure aligns with your business cash flow patterns. Sales-based repayment works best for businesses with consistent card transaction volumes, while those with seasonal fluctuations or heavy cash sales may face repayment strain.

If you experience repayment difficulties, contact your provider to discuss options. Some offer temporary holdback adjustments during documented slow periods, though this extends your repayment timeline and may increase total costs. Managing Clover Capital repayments effectively requires ongoing attention to your sales patterns and proactive communication with your funding partner.

Pro Tip: Use Clover's dashboard reporting tools to create weekly sales forecasts that include your holdback deductions. This visibility helps you anticipate available cash for other expenses and prevents overdrafts or missed vendor payments.

Discover flexible working capital solutions with Clover Capital

Now that you understand how to apply for and manage working capital through Clover POS systems, consider whether Clover Capital merchant cash advance solutions fit your business needs. Clover Capital specializes in providing rapid approval decisions, often within 15 minutes, specifically for merchants using Clover POS systems. This focused approach means underwriting teams understand your industry and transaction patterns intimately.

The platform's flexible repayment structure aligns with your daily sales, removing the burden of fixed monthly payments that strain cash flow during slower periods. Whether you need capital for inventory purchases, equipment upgrades, marketing campaigns, or seasonal staffing, Clover Capital offers funding solutions designed around how your business actually operates. Explore your eligibility and available funding amounts through a quick online application that leverages your existing Clover processing data for faster decisions.

Pro Tip: Visit the dedicated Clover Capital repayment options page to fully understand the flexible repayment structures available and how they adapt to your business's unique sales patterns throughout the year.

Frequently asked questions

How quickly can I receive working capital funds with Clover Capital?

Funding can be approved and dispatched within 72 hours, with many merchants receiving approval decisions in under 24 hours. The speed depends on application completeness and your processing history. Once approved, funds typically transfer to your business bank account within one business day, giving you rapid access to capital when opportunities arise.

What are the eligibility criteria for a Clover working capital advance?

Active Clover account with consistent credit card processing plus a U.S.-based business bank account are required to qualify. Most providers look for at least three to six months of processing history showing stable or growing sales volumes. Exact thresholds vary by issuer, your state, and industry risk factors, but consistent card sales remain the primary qualification factor.

How is repayment calculated and collected on a Clover cash advance?

Repayment is based on a small percentage of daily credit card sales processed on Clover devices, typically 8% to 20%, automatically deducted until paid off. This means repayment varies daily based on your actual sales volume, fitting your cash flow naturally. On high-sales days, more goes toward repayment, accelerating payoff. On slower days, less is collected, preserving working capital. No fixed monthly payments means repayment scales with your business's performance. Review Clover Capital repayment options to understand how different holdback percentages impact your available cash.

Is a merchant cash advance right for every Clover POS business?

Steady card sales are essential for smooth repayments via merchant cash advances. MCAs suit businesses with consistent credit card sales but may strain cash flow for those with volatile or mostly cash transactions. Businesses with seasonal revenue fluctuations should carefully assess whether holdback percentages remain manageable during slow periods. If your sales vary dramatically month to month or you process primarily cash transactions, traditional term loans with fixed payments might provide more predictable cash flow management.