Many Clover POS merchants believe quick business loans are difficult to obtain and confusing to navigate. That's far from the truth in 2026. Quick approval business loans, especially Merchant Cash Advances tied to your Clover system, offer fast funding based on your daily sales. This article breaks down how these loans work, what they cost, how repayment functions, and how to choose the right option. You'll walk away with clear, actionable knowledge to fuel your business growth confidently.

Table of Contents

- How Quick Approval Business Loans Work For Clover POS Merchants

- Understanding Merchant Cash Advances: Costs, Factor Rates, And Repayment

- Comparing Clover MCAs With Alternative Financing Options

- Applying For Quick Approval Business Loans With Clover: Practical Tips

- Get Fast Funding With Clover Capital And CapClover

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Fast approval timeline | Approvals typically happen within 1-2 business days for Clover merchants, with funds available shortly after. |

| Flexible repayment structure | Repayment is tied to a percentage of your daily card sales, adjusting automatically with revenue fluctuations. |

| Higher costs than traditional loans | MCAs use factor rates that can result in effective APRs exceeding 40%, making them costlier than conventional financing. |

| Eligibility requirements | You need at least 6 months in business and 90 days processing with Clover or its partners to qualify. |

| Compare before committing | Evaluate multiple financing options using tools like comparison tables to find the best fit for your cash flow and cost tolerance. |

How quick approval business loans work for Clover POS merchants

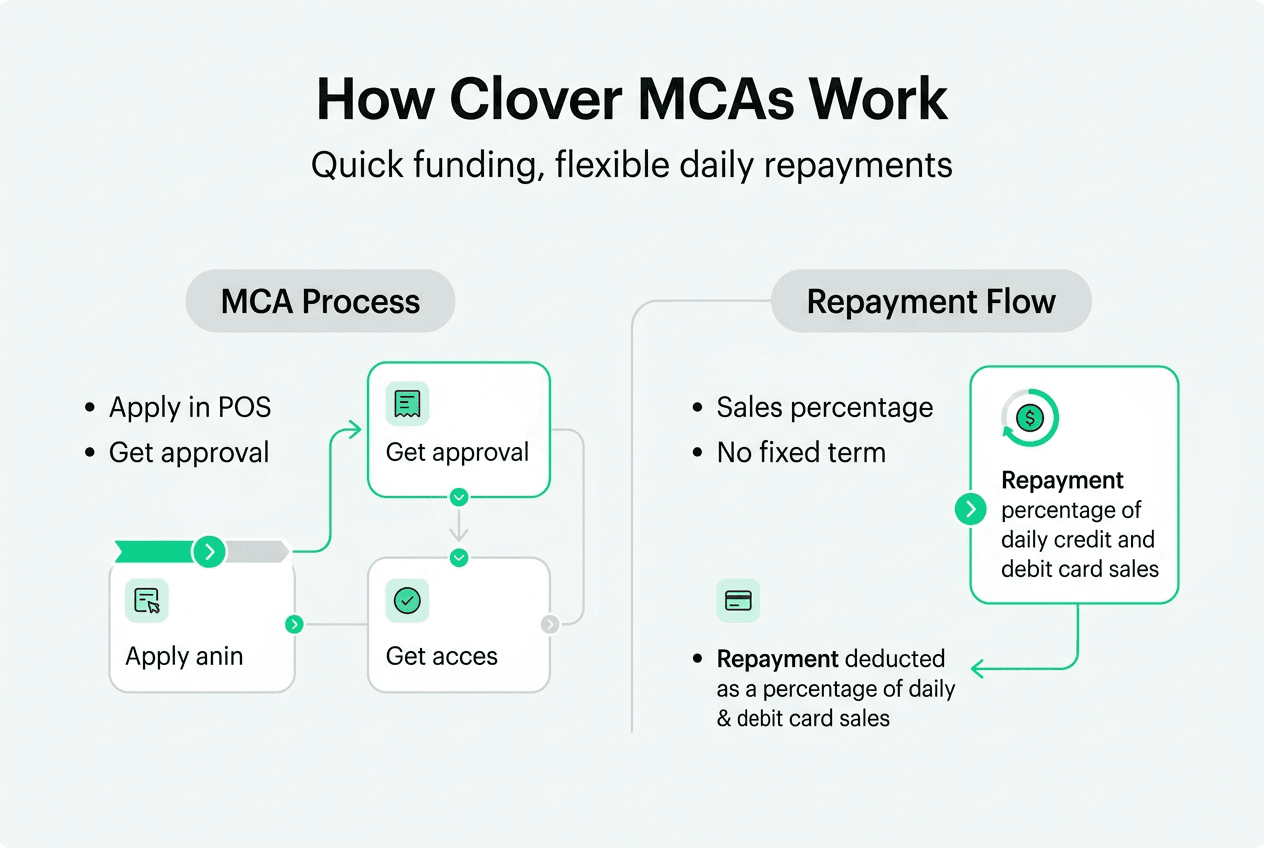

Quick approval loans for Clover merchants convert your future credit card sales into immediate working capital. These loans, often structured as Merchant Cash Advances, leverage your payment processing history to make fast funding decisions. Clover Capital offers quick approval for business loans, with approvals typically taking 1-2 business days after you submit your application through the Clover POS interface or partner platforms.

Once approved, working capital is available in the bank account in 2-3 business days, giving you rapid access to funds for inventory, payroll, or marketing campaigns. The speed comes from the data-driven approval process. Your Clover system tracks daily sales volumes, transaction counts, and processing patterns. Lenders use this real-time data to assess your ability to repay, eliminating lengthy underwriting and documentation requirements.

Eligibility is straightforward but firm. Clover Capital is available to merchants who have been processing with BankTech or its partners for at least 90 days and must be in business for at least 6 months to be eligible. These thresholds ensure you have established sales history and operational stability. If you meet these criteria, the application process is seamlessly integrated into your Clover dashboard.

Repayment works differently than traditional loans. Instead of fixed monthly payments, lenders withhold a percentage of your future daily card sales until the advance is fully repaid. This structure aligns payments with your cash flow. High sales days mean higher repayments, while slower days reduce the burden. It's a flexible model designed for businesses with variable revenue.

The convenience factor is significant. You don't need to visit a bank, fill out extensive paperwork, or wait weeks for decisions. Everything happens within the Clover ecosystem you already use daily. This integration saves time and reduces friction, making it an attractive option for busy merchants.

Pro Tip: Before applying, review your comparison table to understand how different lenders structure their offers. Small differences in factor rates and holdback percentages can significantly impact your total repayment amount.

Key features of Clover quick approval loans:

- Application submitted directly through Clover POS or partner portals

- Approval decisions based on processing history, not traditional credit scores

- Funding deposited within 2-3 business days of approval

- Repayment automatically deducted from daily card sales

- No fixed monthly payment schedule

- Minimal documentation required compared to bank loans

Understanding merchant cash advances: costs, factor rates, and repayment

Merchant Cash Advances charge factor rates instead of interest rates, creating a fundamentally different cost structure. Factor rates typically range from 1.1 to 1.5, meaning you repay 1.1 to 1.5 times the amount you borrow. If you receive $10,000 with a 1.3 factor rate, you'll repay $13,000 total. This fixed repayment amount doesn't change regardless of how quickly you pay it back.

The challenge is understanding the true cost. Factor rates, typically 1.1 to 1.5, create a fixed repayment amount that can translate to APRs over 40%. If you repay that $10,000 advance in three months, your effective APR could exceed 100%. The faster you repay, the higher the annualized cost becomes. MCAs can be more expensive than traditional loans due to factor rates, especially if repayment takes longer than anticipated.

Repayment flexibility is the trade-off for these higher costs. Repayment fluctuates with daily sales volumes, which adds flexibility but can increase effective costs. Your lender withholds a fixed percentage of each day's credit and debit card sales. If you process $1,000 in card sales and your holdback rate is 15%, the lender takes $150 that day. On a $500 sales day, they take $75. This automatic adjustment protects you during slow periods but extends repayment during low sales stretches.

Advantages of this structure include alignment with cash flow and no fixed payment deadlines. You won't default by missing a payment date because there isn't one. Payments happen automatically as you make sales. This works well for seasonal businesses or those with unpredictable revenue patterns. Restaurants, retail stores, and service businesses often benefit from this flexibility.

Risks exist, particularly the potential for a debt spiral. If sales decline significantly, repayments slow, and you might be tempted to take another advance to cover operating expenses. Stacking multiple MCAs creates compounding holdback percentages that can consume 30-50% of daily sales, leaving insufficient cash for operations. High costs of MCAs due to factor rates have contributed to small business bankruptcies when merchants couldn't manage multiple simultaneous advances.

Pro Tip: Calculate the effective APR before accepting any MCA offer. Divide the total cost by the advance amount, then annualize based on expected repayment time. Compare this rate to alternatives like Clover Capital repayment options to ensure you're making an informed decision.

| Factor Rate | Advance Amount | Total Repayment | Cost | Estimated APR (6 months) |

|---|---|---|---|---|

| 1.1 | $10,000 | $11,000 | $1,000 | 20% |

| 1.3 | $10,000 | $13,000 | $3,000 | 60% |

| 1.5 | $10,000 | $15,000 | $5,000 | 100% |

Understanding these mechanics helps you evaluate whether the convenience and speed justify the cost for your specific situation.

Comparing Clover MCAs with alternative financing options

Merchant Cash Advances aren't your only option for quick capital. Traditional small business loans and lines of credit offer lower interest rates, typically 6-12% APR for qualified borrowers. Banks and credit unions require stronger credit profiles, usually scores above 680, and prefer businesses with at least two years of operating history. The application process takes weeks, involves extensive documentation, and often requires collateral or personal guarantees.

Revenue-based financing offers a middle ground. RBF financing offers transparent factor rates from 1.2x to 1.5x and suits businesses with steady revenues and credit scores above 650. Like MCAs, RBF ties repayment to revenue, but it typically uses monthly rather than daily payments and provides more transparent cost structures. RBF lenders often cap total repayment amounts and offer clearer timelines, making it easier to budget and plan.

SBA loans provide the lowest rates, often 5-8% APR, but require extensive documentation, strong credit, and collateral. The approval process can take 60-90 days, making them unsuitable for urgent needs. However, for long-term investments like equipment purchases or real estate, SBA loans offer unbeatable value. Consider alternatives like traditional small business loans, lines of credit, or SBA loans as potentially cheaper options when you have time to wait and meet credit requirements.

MCAs excel in specific scenarios. They accept lower credit scores, sometimes as low as 500, and emphasize daily sales volume over credit history. If you've been denied by banks due to credit issues or lack of collateral, MCAs provide access to capital that might otherwise be unavailable. The speed is unmatched for urgent needs like emergency equipment repairs, seasonal inventory purchases, or unexpected tax bills.

The choice depends on four factors: credit profile, cash flow stability, urgency of funds, and cost tolerance. Strong credit and stable revenue favor traditional loans. Urgent needs with acceptable credit favor MCAs. Long-term investments with time to wait favor SBA loans. Understanding your priorities helps you select the right tool for your situation.

Pro Tip: Use best Clover Capital alternatives to compare multiple lenders side by side. Look beyond factor rates to holdback percentages, funding speed, and customer reviews to find the best overall package.

| Financing Type | Approval Time | Typical Cost | Credit Requirements | Best For |

|---|---|---|---|---|

| Merchant Cash Advance | 1-2 days | 40-100%+ APR | 500+ score | Urgent needs, variable revenue |

| Revenue-Based Financing | 3-5 days | 20-40% APR | 650+ score | Steady revenue, moderate urgency |

| Traditional Bank Loan | 2-4 weeks | 6-12% APR | 680+ score | Long-term investments, strong credit |

| SBA Loan | 60-90 days | 5-8% APR | 680+ score, collateral | Major investments, lowest cost priority |

Applying for quick approval business loans with Clover: practical tips

Before applying, verify your eligibility. You need at least six months in business and 90 days processing with Clover or its partners. Check your Clover dashboard to confirm your processing history meets this threshold. Review your daily sales trends to understand what advance amount you can realistically repay without straining cash flow.

Step 1: Log into your Clover POS system and navigate to the capital or funding section. Some merchants access this through the main dashboard, while others find it under business tools or financial services. If you can't locate it, contact Clover support or check with your payment processor, as access methods vary by partnership arrangement.

Step 2: Review your sales history for accuracy. The application process is streamlined and integrated into Clover POS systems, relying on your sales history. Lenders use this data to determine your advance amount and holdback percentage. Ensure your processing data is complete and reflects your actual sales volumes. Discrepancies can delay approval or result in lower offers.

Step 3: Submit required documentation. You'll typically need your business tax ID, bank account information for fund deposits, and basic business details like address and ownership structure. Some lenders request additional documents like bank statements or tax returns, but Clover-integrated applications minimize these requirements by leveraging your processing data.

Step 4: Await quick approval, typically within 1-2 business days. During this time, the lender analyzes your sales patterns, calculates risk, and determines your offer. You'll receive notification through email or your Clover dashboard. Review the offer carefully, paying attention to the factor rate, holdback percentage, and estimated repayment timeline.

Step 5: Understand repayment terms before accepting. Calculate the total repayment amount by multiplying your advance by the factor rate. Estimate how long repayment will take based on your average daily sales and holdback percentage. If a 15% holdback on $2,000 daily sales means $300 daily payments, and you owe $13,000, expect roughly 43 days to full repayment, though this will vary with sales fluctuations.

Step 6: Compare multiple offers using your comparison table. Don't accept the first offer you receive. Small differences in terms can save thousands of dollars. Look for the lowest factor rate, reasonable holdback percentages that won't strain operations, and lenders with strong customer service reputations.

Pro Tip: Calculate effective APRs for each offer to compare apples to apples. Factor rates obscure true costs, but converting to APR reveals which deal is genuinely better. Use online calculators or spreadsheets to model different scenarios based on optimistic, realistic, and pessimistic sales projections.

Common application mistakes to avoid:

- Applying for more than you need, increasing total costs unnecessarily

- Ignoring the holdback percentage impact on daily cash flow

- Failing to compare multiple lenders before accepting an offer

- Overlooking early repayment terms that might save costs

- Not reading the fine print about additional fees or renewal terms

- Accepting offers without calculating effective APR

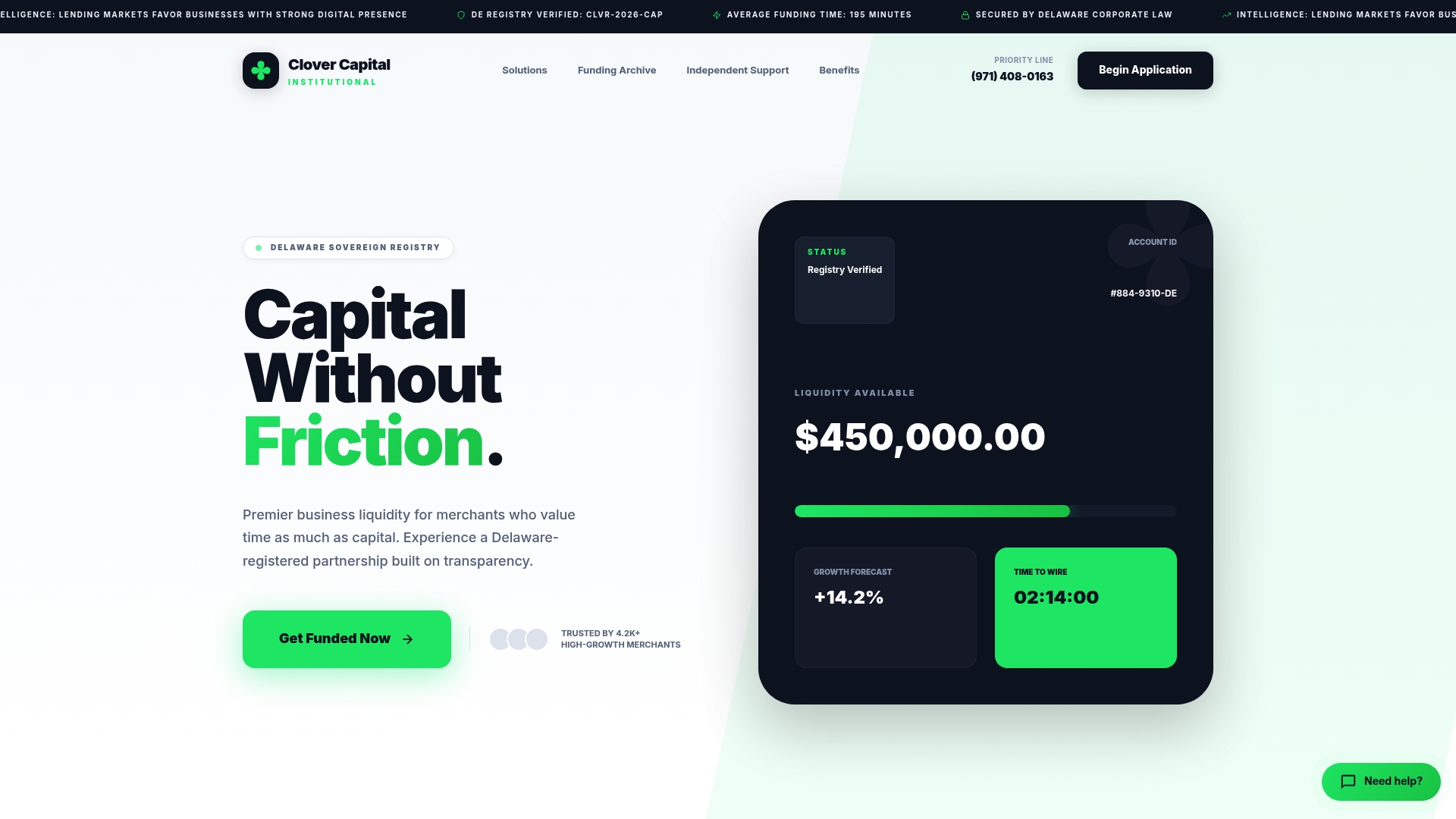

Get fast funding with Clover Capital and CapClover

If you're ready to secure working capital quickly, CapClover offers tailored merchant cash advances designed specifically for Clover POS users. Our streamlined application integrates directly with your Clover processing data, delivering Clover Capital MCA 15-min approval decisions without lengthy paperwork or credit checks. You'll get transparent factor rates, flexible repayment tied to your daily sales, and funding in your account within days.

Compare CapClover and Clover Capital side by side using our detailed Clover vs CapClover comparison to find the best fit for your business needs. Whether you need inventory capital for retail, working capital for hospitality, or marketing funds for digital commerce, we provide solutions that adapt to your revenue patterns. Explore answers to common questions about Clover Capital repayment questions to understand exactly how payments work and what to expect throughout the funding relationship.

Frequently asked questions

How long does quick approval take for Clover business loans?

Approvals typically take 1-2 business days after you submit your application through the Clover POS system or partner platforms. Once approved, funds are deposited into your bank account within 2-3 business days, giving you access to working capital in less than a week from application to funding. This speed comes from automated underwriting that analyzes your Clover processing history rather than requiring manual document review.

What eligibility criteria must I meet to qualify for Clover Capital?

Merchants must have 90 days processing with Clover or partners and 6 months in business to qualify for quick approval loans. These requirements ensure you have established sales history and operational stability that lenders can evaluate. Your daily credit and debit card processing volumes determine your advance amount, with higher consistent sales qualifying for larger funding offers.

Are merchant cash advances more expensive than traditional loans?

Yes, MCAs often have effective APRs over 40%, significantly higher than traditional bank loans that typically range from 6-12% APR. The higher cost reflects the speed, convenience, and accessibility MCAs offer to merchants with lower credit scores or limited collateral. Factor rates create fixed repayment amounts that translate to higher annualized costs, especially when repayment occurs quickly due to strong sales volumes.

Can I repay Clover MCA early to save costs?

Early repayment policies vary by lender and specific agreement terms. Some MCAs use fixed factor rates that don't decrease with early repayment, meaning you pay the same total amount regardless of timeline. Others offer discounts for early payoff, reducing your total cost if you can accelerate repayment. Review your contract carefully or ask your lender directly about early repayment provisions before accepting an offer.

Is repayment amount fixed or does it change with sales?

Repayment fluctuates as a percentage of daily card sales, adjusting automatically with your revenue. Higher sales days result in larger repayments, while slower days reduce the amount withheld. This flexibility protects your cash flow during slow periods but can extend total repayment time if sales decline. The total amount you repay remains fixed based on your factor rate, but daily payment amounts vary with transaction volumes.