Small businesses often need capital fast, yet traditional bank loans can take weeks or even months to approve and fund. Merchant cash advances solve this problem by providing immediate access to working capital, often within 24 to 48 hours. Unlike conventional loans, MCAs purchase a portion of your future sales and repay through a percentage of daily revenue, creating a flexible payment structure that scales with your business performance. For Clover POS merchants, this funding model integrates seamlessly with existing payment processing, making it an increasingly popular choice for growth capital. This guide explains exactly how merchant cash advances work, their costs and risks, and how Clover merchants can leverage them effectively.

Table of Contents

- Understanding Merchant Cash Advances: How They Work

- Clover Cash Advance: Tailored MCA Solutions For POS Merchants

- Costs, Risks, And Regulations Of Merchant Cash Advances

- Practical Tips For Small Businesses Considering Merchant Cash Advances

- Find Flexible Merchant Cash Advance Options With Clover Capital

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| MCAs purchase future sales | Merchant cash advances are not loans but purchases of future receivables, repaid through daily sales. |

| Flexible repayment structure | Payments automatically adjust based on revenue, reducing pressure during slow periods. |

| Fast approval and funding | Most MCAs fund within 24 to 48 hours with approval rates around 84% versus 21.6% for banks. |

| Higher costs than loans | Factor rates can produce implied APRs exceeding 100%, making MCAs expensive compared to traditional financing. |

| Clover integration simplifies process | Clover Cash Advance automates repayment through POS transactions, streamlining the entire funding experience. |

Understanding merchant cash advances: how they work

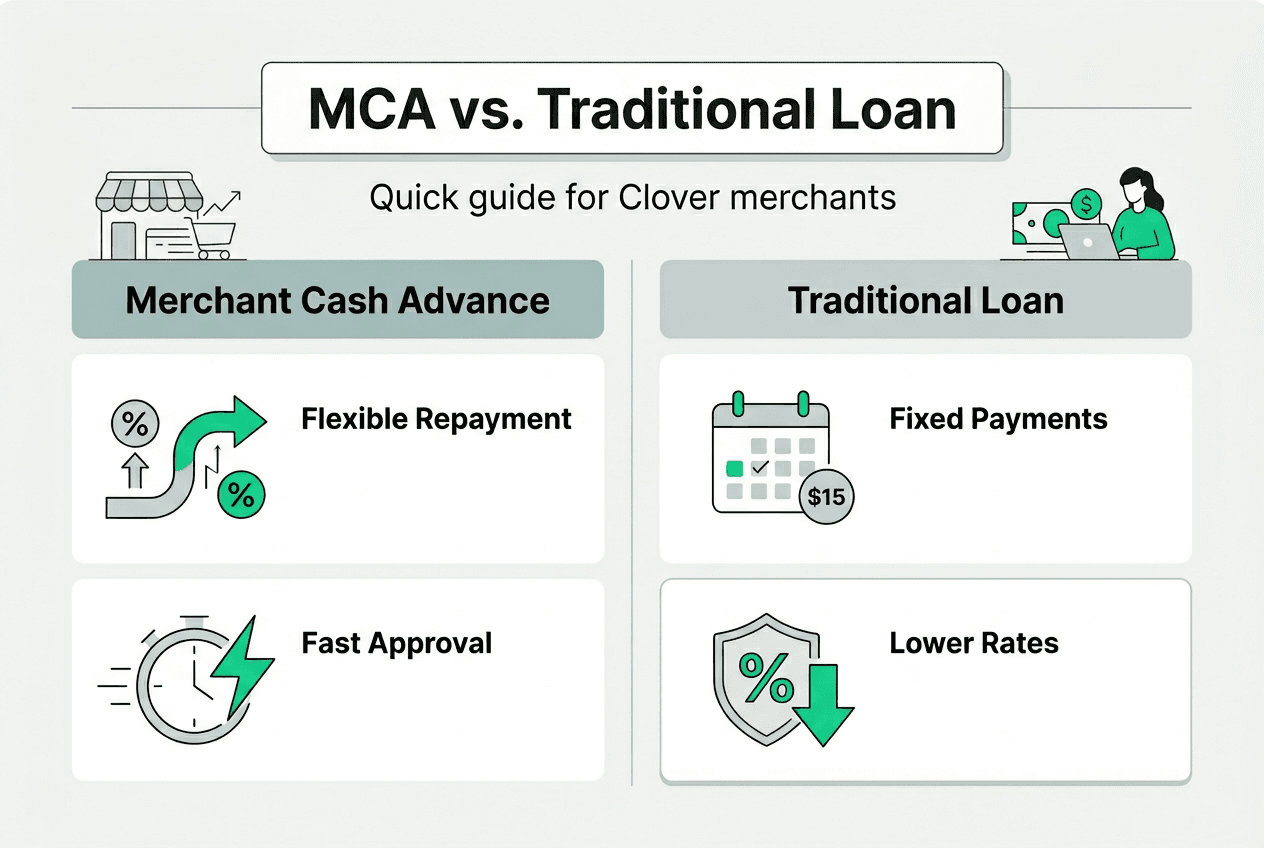

Merchant cash advances represent a fundamentally different approach to business financing. Instead of borrowing money and repaying it with interest, you sell a portion of your future credit card receivables to a funding company in exchange for immediate capital. The provider then collects repayment by taking a fixed percentage of your daily or weekly sales until the advance is fully repaid.

This repayment structure creates natural flexibility. When sales are strong, you repay faster. During slower periods, your payments automatically decrease because they're tied directly to revenue. MCAs provide quick capital often within 24 to 48 hours, making them ideal for urgent needs like inventory purchases, equipment repairs, or marketing campaigns.

Approval rates tell an important story. Traditional bank loans approve roughly 21.6% of small business applications, while MCAs approve approximately 84%. This dramatic difference stems from how providers evaluate risk. Instead of focusing primarily on credit scores and collateral, MCA providers analyze your processing history and daily sales volume. If you consistently process card transactions, you're likely to qualify.

MCAs use factor rates instead of interest rates to determine costs. A factor rate typically ranges from 1.1 to 1.5, meaning you repay $1,100 to $1,500 for every $1,000 advanced. The holdback percentage, usually between 10% and 20% of daily sales, determines how quickly you repay. Automated systems deduct this percentage directly from your card processing, eliminating the need for manual payments.

Pro Tip: Review your last three months of sales data before applying to estimate your daily holdback amount and ensure it won't strain your working capital.

For Clover Capital merchant cash advance users, integration with existing POS systems makes the entire process seamless. Repayments happen automatically as you process transactions, and funding decisions rely on real sales data already flowing through your Clover account.

Clover cash advance: tailored MCA solutions for POS merchants

Clover Cash Advance offers merchant cash advances specifically designed for businesses using Clover POS systems. This integration creates unique advantages by linking funding decisions and repayment directly to your existing payment processing infrastructure.

Eligibility requirements focus on practical business metrics rather than perfect credit scores. You typically need an active Clover account processing a minimum monthly volume, usually around $5,000 to $10,000 in card sales. Geographic restrictions may apply, with availability varying by state. Certain high risk industries like gambling, adult entertainment, or cryptocurrency may face restrictions due to regulatory and risk considerations.

Clover Cash Advance provides capital within a few business days with repayments scaling on card sales, creating predictable cash flow management. The automated deduction process means you never miss a payment or need to remember due dates. Each time a customer swipes their card, a predetermined percentage goes toward your advance repayment while the remainder deposits into your business account.

Holdback rates typically range from 10% to 20% of daily card transactions. A 15% holdback on $1,000 in daily sales means $150 goes to repayment and $850 to your account. This percentage remains constant regardless of sales volume, so higher revenue days accelerate repayment while slower days extend the timeline.

Funding speed represents a critical advantage. After approval, most Clover merchants receive funds within one to three business days. This timeline beats traditional loans by weeks or months, making MCAs practical for time sensitive opportunities like bulk inventory discounts or urgent equipment replacements.

Pro Tip: Keep sales data updated on your Clover system to maintain smooth repayment processing and avoid reconciliation issues.

Understanding Clover Capital repayment options helps you plan for different business scenarios. If you anticipate seasonal fluctuations, confirm how repayment adjusts during slower months. Some providers offer temporary holdback reductions during documented downturns, while others maintain fixed percentages regardless of circumstances.

For merchants comparing Clover Capital funding speed alternatives, evaluate not just approval timelines but also how quickly funds actually reach your account after approval. Same day funding exists but often comes with higher costs or stricter requirements.

Costs, risks, and regulations of merchant cash advances

Merchant cash advances carry significantly higher costs than traditional loans, primarily due to their structure and risk profile. MCAs use factor rates instead of interest, which can produce very high implied APRs up to 350%, making them one of the most expensive forms of business financing available.

Factor rates work differently than interest rates. A 1.3 factor rate on a $10,000 advance means you repay $13,000 total, regardless of how long repayment takes. If you repay in three months, the implied APR exceeds 100%. If repayment stretches to 12 months, the effective rate drops but remains substantially higher than conventional loans.

Regulatory oversight remains minimal because MCAs are structured as purchases of future receivables rather than loans. This classification exempts them from state usury laws that cap interest rates on traditional lending. The Yale article on MCA regulation details how this regulatory gap allows providers to charge rates that would be illegal for licensed lenders.

Some states have begun requiring specific disclosures, including estimated APR calculations and total repayment amounts. California, New York, and Utah have implemented transparency laws, but enforcement varies and many providers operate across state lines, complicating regulatory jurisdiction.

Default risks have increased substantially. Merchant cash advance defaults surged 59% to $2.2 billion in 2024, reflecting both aggressive lending practices and challenging economic conditions for small businesses. When merchants stack multiple MCAs, the combined holdback percentages can consume 40% to 60% of daily revenue, creating unsustainable cash flow pressure.

| Feature | Merchant Cash Advance | Traditional Loan |

|---|---|---|

| Approval rate | 84% | 21.6% |

| Funding speed | 24 to 48 hours | 2 to 8 weeks |

| Cost structure | Factor rate 1.1 to 1.5 | APR 6% to 12% |

| Repayment | % of daily sales | Fixed monthly |

| Collateral required | None | Often required |

Repayment structures vary between providers. Some use fixed daily or weekly withdrawals regardless of sales volume, functioning more like short term loans. Others use true percentage based holdbacks that flex with revenue. The Clover Capital comparison details page shows how different structures impact total costs and repayment timelines.

Pro Tip: Carefully review your merchant agreement and factor rate implications before signing, paying special attention to confession of judgment clauses that allow providers to claim assets without court proceedings.

Stacking multiple MCAs creates compounding risk. Each additional advance adds to your daily holdback percentage, reducing available working capital. When combined holdbacks exceed 30% to 40% of revenue, businesses often struggle to cover operating expenses, leading to defaults or forced closures.

Practical tips for small businesses considering merchant cash advances

Successful MCA use requires careful planning and realistic assessment of your business finances. Start by analyzing your average daily sales over the past six months, identifying seasonal patterns and typical revenue fluctuations. This baseline helps you estimate sustainable holdback percentages that won't strain operations during slower periods.

Follow these steps when preparing to apply:

- Calculate your average daily card sales for the past 90 days using Clover reporting tools.

- Multiply this average by your anticipated holdback percentage to estimate daily repayment amounts.

- Subtract this amount from your average daily revenue to confirm sufficient remaining cash flow for expenses.

- Review your current outstanding debts and obligations to avoid over leveraging.

- Gather required documentation including bank statements, processing history, and business tax returns.

Compare multiple MCA offers before committing. Request detailed breakdowns showing total repayment amount, factor rate, holdback percentage, and estimated repayment timeline. Some providers advertise low factor rates but compensate with high origination fees or extended repayment periods that increase total costs.

Track all repayment deductions carefully through your Clover dashboard. Automated systems occasionally malfunction or apply incorrect holdback percentages, creating unexpected cash flow shortfalls. Regular monitoring helps you catch discrepancies early and maintain accurate financial records.

Prioritize providers offering transparent terms and flexible repayment options. Red flags include confession of judgment clauses, aggressive collection practices, or reluctance to provide written disclosure of all costs and terms. Legitimate providers should clearly explain every aspect of the agreement without pressure tactics.

Earlier evaluation of payment stack allows for more restructuring options and reduces risk of default. If you already have one or more MCAs, assess your total holdback percentage immediately. Combined deductions exceeding 35% of revenue signal serious risk requiring professional consultation or restructuring.

Pro Tip: Maintain good sales processing records in Clover POS for smooth approval and repayment, ensuring all transactions are properly categorized and reconciled daily.

Ask these essential questions before signing any MCA agreement:

- What is the total repayment amount in dollars, not just the factor rate?

- How is the holdback percentage calculated, and can it change?

- What happens if my sales drop significantly for an extended period?

- Are there prepayment penalties or benefits for early repayment?

- Does the agreement include confession of judgment or personal guarantee clauses?

- What specific circumstances trigger default, and what are the consequences?

Consider alternatives before committing to an MCA. Business lines of credit, SBA loans, or equipment financing often provide capital at significantly lower costs. MCAs work best for short term needs where speed justifies the premium, not as ongoing working capital solutions.

When ready to apply for Clover Capital MCA, ensure your Clover account shows consistent processing history with minimal chargebacks or disputes. Clean transaction records improve approval odds and may qualify you for better rates.

Find flexible merchant cash advance options with Clover Capital

Now that you understand how merchant cash advances work, their costs, and best practices for responsible use, you can explore funding options tailored specifically for Clover merchants. Clover Capital MCA solutions offer fast approval processes, often delivering decisions within 15 minutes and funding within one to two business days.

Repayment automatically scales with your sales volume, helping you manage cash flow during seasonal fluctuations or unexpected slowdowns. Dedicated support teams answer questions about Clover Capital repayment options, eligibility requirements, and application processes. Whether you need inventory capital, equipment upgrades, or marketing funds, exploring Clover MCA funding alternatives helps you find the right partner for your business growth.

Frequently asked questions

What happens if I can't keep up with merchant cash advance payments?

MCA providers typically deduct payments automatically as a percentage of your daily sales, so payments naturally decrease when revenue drops. However, if sales fall so low that you can't meet minimum operating expenses after holdbacks, you risk default. Contact your provider immediately to discuss restructuring options or temporary holdback reductions before missing payments triggers collection actions.

Are merchant cash advances regulated like traditional loans?

MCAs are structured as purchases of future receivables, not loans, exempting them from most lending regulations including state usury laws. This classification means less oversight and consumer protection compared to traditional financing. Some states like California and New York require specific disclosures, but federal regulation remains minimal, creating a largely self regulated industry.

How quickly can I get funding after applying for a merchant cash advance?

Most MCA providers fund within 24 to 48 hours after approval, with some offering same day deposits for qualified applicants. Clover Cash Advance typically delivers funds within one to three business days, significantly faster than traditional loans requiring weeks or months. Pre qualification often needs minimal documentation since providers primarily evaluate your processing history rather than extensive financial statements.

Can I have multiple merchant cash advances at the same time?

Yes, but stacking multiple MCAs creates substantial risk by increasing your total daily holdback percentage. Combined deductions exceeding 35% to 40% of revenue often create unsustainable cash flow pressure, leading to defaults. Each additional MCA also typically carries higher costs since providers view stacked advances as increased risk, charging premium factor rates to compensate.

Do merchant cash advances affect my business credit score?

Most MCA providers don't report to business credit bureaus during normal repayment, so timely payments typically don't improve your score. However, defaults or legal actions resulting from non payment will damage your credit significantly. Some providers conduct hard credit inquiries during application, which may temporarily lower your score by a few points.